Together with…

The Microcredit Market

In the vast landscape of finance, microcredit stands as a beacon of hope for millions. Imagine a world where starting a small business, escaping poverty, and empowering oneself seems like a distant dream. Microcredit shatters that illusion. It’s a financial lifeline, offering small loans to low-income individuals who lack access to traditional banking services. This innovative approach allows them to invest in their ideas, build businesses, and create a brighter future for themselves and their families.

Microcredit isn’t just about money; it’s about unlocking potential, fostering self-reliance, and driving positive change at the grassroots level. From bustling market stalls to local workshops, microcredit fuels the dreams of countless individuals, paving the way for a more inclusive and equitable global economy.

Empowering Potential: How Microcredit Works

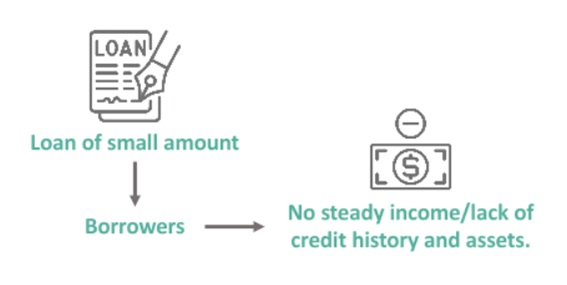

Microcredit offers a unique lifeline to those striving to rise above poverty in developing economies. It’s built on the belief that impoverished communities harbor individuals with entrepreneurial spirit and valuable skills, but lack access to traditional financial services that can nurture their ambitions.

Imagine a world where bartering, the exchange of goods and services, is the primary economic system. Microcredit disrupts this by introducing small loans, starting from as low as $200 through Microfinance Institutions (MFIs) or Non-Governmental Organizations (NGOs). These loans are designed specifically for individuals who wouldn’t qualify for traditional bank loans.

The process is streamlined and often bypasses written contracts. Repayment starts immediately, building a sense of accountability from the outset. As borrowers successfully repay their loans, they establish a credit history, paving the way for access to larger loans in the future. This creates a cycle of empowerment.

Here’s a closer look at the inner workings of microcredit:

- Borrower Assessment: MFIs don’t rely solely on traditional credit scores. They conduct a thorough assessment, evaluating a potential borrower’s ability to repay the loan, the viability of their business idea, and their social background to determine their commitment and support network.

- Loan Disbursement: Once approved, borrowers receive the loan amount. This critical step is often accompanied by financial literacy training and mentorship. These resources equip borrowers with the knowledge and skills to manage their finances effectively and maximize the impact of the loan on their business.

- Repayment: Microcredit loans typically come with affordable interest rates and are structured with regular installments over a set timeframe. This repayment structure is designed to be manageable for low-income borrowers and fosters a sense of responsibility.

- Credit History Building: Successful repayment is the cornerstone of microcredit’s success. Each on-time payment builds the borrower’s credit history, opening doors to larger loans and future financial opportunities. This empowers them to invest in their businesses, create jobs, and ultimately, break the cycle of poverty.

Microcredit goes beyond simply providing financial resources. It’s a catalyst for social and economic change, fostering self-reliance, dignity, and a brighter future for countless individuals and their communities.

CLICK HERE TO GET MORE INFORMATION

Tailored Solutions: Exploring Different Types of Microcredits

Microcredit isn’t a one-size-fits-all solution. To cater to diverse needs and goals, various microcredit programs have emerged:

- Micro Loans: This is the foundation of microcredit, offering small loans to individuals who wouldn’t qualify for traditional bank loans. These loans don’t require collateral and are specifically designed to support new or small businesses.

- Micro Savings: This program encourages a savings habit among low-income individuals. Microfinance institutions offer special savings accounts with no minimum balance requirement. These accounts often accrue interest, incentivizing saving and fostering financial responsibility.

- Micro Insurance: Traditional insurance plans can be cost-prohibitive for low-income individuals. Micro Insurance addresses this gap by offering basic insurance coverage at a significantly lower premium compared to standard policies. This provides borrowers with financial protection against unforeseen events like illness or accidents.

- Agricultural Loans: As the name suggests, these loans are specifically designed to meet the needs of farmers and agricultural businesses. They can be used to finance essential purchases like seeds, fertilizers, or equipment, empowering farmers to improve yields and increase their income.

- Group Lending: This model fosters a sense of community and shared responsibility. Borrowers form small groups, and each member acts as a co-guarantor for the loan repayment of others in the group. This provides a safety net for the MFI and incentivizes timely repayments within the group.

- Revolving Loan Fund: This program creates a sustainable lending pool. MFIs establish a fund from which loans are disbursed. As borrowers repay their loans, the funds are cycled back into the pool, allowing the MFI to provide loans to new borrowers. This model ensures the program’s continuity and empowers a larger number of individuals over time.

By offering a variety of microcredit options, MFIs can cater to the specific needs of diverse communities and empower individuals to pursue their entrepreneurial dreams, build a brighter future, and contribute to a more inclusive and thriving economy.

A Powerful Tool with Nuances – A SWOT Analysis

Microcredit has become a cornerstone for poverty alleviation and economic empowerment worldwide. However, it’s not a one-size-fits-all solution, and understanding its strengths, weaknesses, opportunities, and threats is crucial for maximizing its positive impact.

Strengths:

- Financial Inclusion: Microcredit unlocks the doors of the financial system for the unbanked population. It provides access to financial services like loans and savings accounts, fostering self-reliance and enabling individuals to start or grow small businesses. This fosters economic participation and creates a pathway out of poverty.

- Poverty Reduction: By supporting income generation, microcredit empowers individuals and families to break the cycle of poverty. The World Bank has documented examples of how microcredit increases consumption levels and improves living standards, allowing families to invest in education, healthcare, and better housing.

- Women’s Empowerment: Microcredit programs often target women, recognizing their critical role in driving economic development and poverty reduction within households. Access to loans empowers women to gain financial independence, participate more actively in decision-making, and challenge traditional gender roles.

Weaknesses:

- Over-Indebtedness: Predatory lending practices and unrealistic repayment terms can lead to borrower overload, jeopardizing their financial stability. Some borrowers may take on multiple loans from different lenders, making it difficult to manage their debt. The 2010 microfinance crisis in Andhra Pradesh, India, highlighted the dangers of aggressive lending without adequate borrower protection measures.

- Lack of Business Skills: Microcredit recipients often come from underprivileged backgrounds and may lack essential business management skills. This can hinder their ability to effectively utilize the loan, manage their finances, and achieve their business goals.

- High-Interest Rates: Microloans can carry high interest rates to cover operational costs and mitigate risk associated with lending to individuals without collateral. However, these rates can become a significant burden on low-income borrowers, potentially limiting the positive impact of the loan.

Opportunities:

- Technological Innovation: Technological advancements like mobile banking can revolutionize access to financial services for microcredit borrowers. Mobile apps can streamline loan applications, simplify repayment processes, and provide financial literacy resources, all contributing to the success of microcredit programs.

- Impact Investing: Increased investment in microfinance institutions with a focus on social impact alongside financial returns can promote responsible lending practices. Impact investors can encourage MFIs to provide financial literacy training, and business development support, and prioritize borrower well-being.

- Skills Development: Integrating financial literacy training and business skills development programs with microcredit can significantly increase borrowers’ chances of success. Training in areas like budgeting, marketing, and basic accounting equips borrowers with the knowledge and skills necessary to make informed financial decisions, manage their businesses effectively, and ensure loan repayment.

Threats:

- Overly Stringent Regulations: Overly stringent regulations can inadvertently stifle innovation and limit access to microcredit for those who need it most. Regulations should strike a balance between protecting borrowers and allowing MFIs to adapt and develop new loan models to serve diverse needs.

- Economic Downturns: Economic recessions or financial crises can severely impact borrowers’ ability to repay loans, leading to defaults and instability for MFIs. This can disrupt the entire microcredit ecosystem, leaving borrowers vulnerable and limiting access to future loans.

- Unsustainable Practices: Microfinance institutions solely focused on profit maximization may resort to predatory lending practices, harming borrowers. Aggressive collection tactics, high fees, and unrealistic loan terms can trap borrowers in a cycle of debt. Strong ethical guidelines and regulations are needed to ensure MFIs prioritize social impact alongside financial sustainability.

Microcredit remains a powerful tool for financial inclusion and economic development, but its successful implementation requires a nuanced approach. Responsible lending practices, coupled with financial literacy training, business skills development, and addressing potential pitfalls, are crucial for maximizing microcredit’s positive impact. By constantly innovating, promoting ethical practices, and tailoring programs to local needs, microcredit can continue to empower individuals, strengthen communities, and contribute to a more inclusive, equitable, and prosperous world.

Conclusion

Microcredit has become a cornerstone for empowering individuals around the world by fostering entrepreneurship and financial inclusion. Studies showcase its positive impact on income generation, education, healthcare, and even climate change resilience. With its focus on providing access to credit and fostering self-reliance, microcredit has demonstrably improved the lives of millions.

As in any sector, it is necessary to analyse its risks and characteristics in order to fully understand its functioning and its strengths and weaknesses, as well as potential developments and areas for improvement.

CLICK HERE TO GET MORE INFORMATION

Disclaimer

Index:

Data Room AccessData room access is available only for accredited and institutional investors due to FCA permissions.

To gain access, click and fill out the following form. Our compliance team will grant you access within 24 hours.